SMM July 10 Report:

Unlike the significant zinc price rally in the first half of 2024, the main SHFE zinc contract showed a downward trend in the first half of 2025. As of July 10, 2025, the half-yearly decline of the main SHFE zinc contract reached 11.56%. On April 7, the contract hit a half-yearly low of 21,620 yuan/mt, marking a new low in the past year.

Specifically, in early January, the US announced a high inflation rate, leading the market to expect that the US Fed might slow down interest rate cuts. Subsequently, with Trump's assumption of office, the market began to anticipate related political and economic policies in advance. The US dollar index continued to fluctuate at highs, and bearish funds entered the market, putting pressure on zinc prices. On the supply side, the increase in January was relatively limited. Coupled with the limited opening time of the zinc ingot import window in January, the inflow of imported zinc ingots was expected to remain stable, with no significant increase in overall zinc ingot supply. On the consumption side, as the Chinese New Year holiday approached, domestic downstream zinc enterprises gradually began to shut down production for the holiday, with holiday durations ranging from a few days to several tens of days. In January, most downstream enterprises had insufficient production days. Although some enterprises stocked up on zinc ingots before the holiday, overall zinc ingot consumption still declined significantly. The fundamental support for zinc prices was insufficient, coupled with the gradual easing of the domestic zinc ore market, causing zinc prices to decline throughout January. The monthly decline in January was 7.09%.

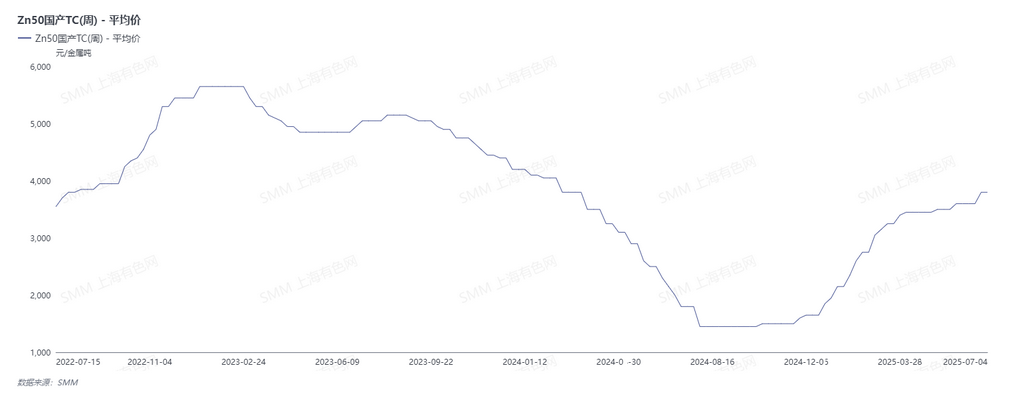

In February, after the holiday, the US implemented a series of tariff policies against China and other countries, continuing to disrupt market sentiment. However, China also proposed to continue expanding the trade-in policy for consumer goods and to further strengthen fiscal and monetary policies. These positive measures improved macro sentiment, providing some support for zinc prices in February. On the supply side, the overall decline in refined zinc production in February was relatively significant. With the continuous increase in zinc concentrate TCs, the profits of domestic smelters gradually recovered, and some smelters have already entered a profitable state. Smelters' willingness to increase production strengthened. However, affected by the Chinese New Year holiday, the downstream resumption of work was slow, and demand for zinc ingots weakened. Overall, the monthly decline in February continued to be 0.97%.

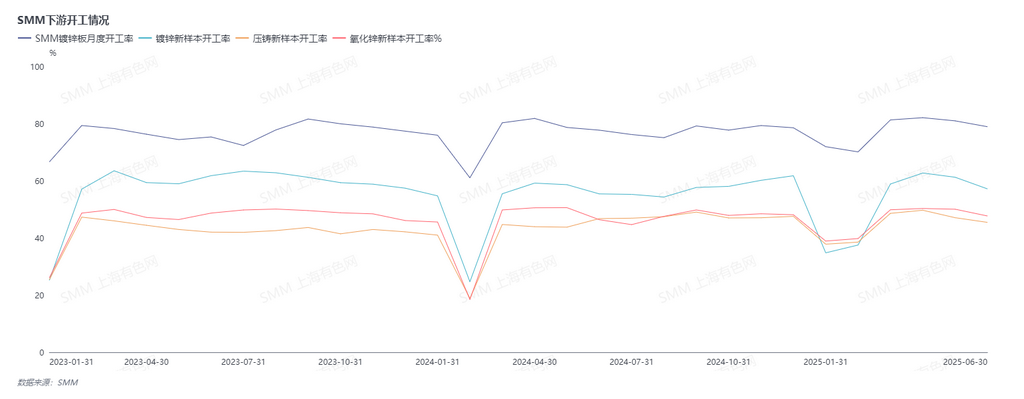

Entering March, internationally, Trump's tariff policies escalated. Domestically, it coincided with the Two Sessions. Apart from the 1.3 trillion yuan special treasury bonds, the policies generally met market expectations, with GDP growth targeted at around 5%, a fiscal deficit ratio of around 4%, moderately loose monetary policies, and timely RRR cuts and interest rate cuts. Overall, domestic policies continued to improve. On the supply side, with domestic mine TCs rising above 3,400 yuan/mt (metal content) and sulphuric acid prices increasing again, smelters' production enthusiasm improved, and maintenance times were postponed, leading to an increase in smelter production. On the consumption side, galvanizing production in March was slightly lower than the same period last year, with limited actual market consumption recovery. However, steel towers and some export orders performed well. Die-casting zinc alloy production varied between large and small factories, with orders more concentrated in large factories. Overall, production was better than the same period last year. Zinc oxide production was relatively stable, with improved consumption and macro sentiment. The monthly increase in March was 0.13%.

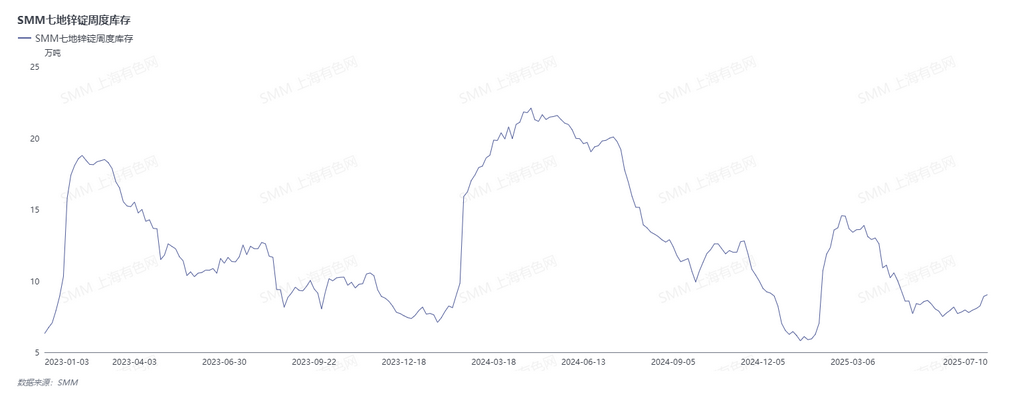

In April, tariff issues resurfaced, with reciprocal tariffs imposed by the US exacerbating international trade uncertainties. Market concerns spread, putting pressure on zinc prices, which fell sharply to yearly lows. Supply side, although TCs struggled to rise and smelter raw material inventories dropped to 27 days, they remained at elevated levels. On the demand side, tariff concerns triggered an export rush and early release of future demand, boosting operating rates. However, the macro impact of tariffs persisted, with zinc prices closing down 4.33% for the month.

In May, China and the US initiated negotiations, easing trade tensions. Domestically, while a series of RRR cuts and interest rate cuts were announced, they largely met expectations without significant surprises. Mid-month, the negotiation outcome was released, showing substantial tariff reductions between the two nations. Improved macro sentiment drove zinc prices higher, but as market sentiment gradually digested the news, macro influences waned, and zinc prices resumed a fluctuating trend. Supply side, driven by sulphuric acid profits, some smelters increased production. Coupled with a substantial inflow of imported zinc ingots into the domestic market in May, overall zinc ingot supply remained high. With the easing of Sino-US tariff conflicts, downstream enterprises resumed production of previously suspended export orders, keeping overall orders and consumption robust. However, limited new export orders and a pullback in some domestic trade orders meant downstream zinc consumption showed no growth MoM. Amid oversupply, zinc prices closed down 0.96% for May.

In June, geopolitical risks initially rose, increasing trade uncertainty, but later subsided. Weak US economic data led to a pullback in the US dollar index and Treasury yields, boosting expectations for US Fed interest rate cuts. A phone call between Chinese and US leaders fueled market optimism, while the central bank's trillion-yuan reverse repo operations signaled clear intent to boost domestic demand via liquidity injection. Concurrently, at the Shanghai Lujiazui Forum, the central bank unveiled eight policy measures to support Shanghai's international financial center development, focusing on monetary policy and fostering warm macro sentiment. As smelters continued to release new capacity and maintenance-plagued enterprises gradually resumed operations, coupled with lower electricity costs in some regions entering the rainy season, sulphuric acid and minor metal profits remained high YoY, sustaining strong production incentives. The upward trend in refined zinc output persisted. Demand side, rising temperatures and the onset of the rainy season constrained infrastructure project progress, while end-user orders across sectors declined. Existing export orders continued to be digested, and domestic demand weakened. Overall, downstream zinc consumption gradually declined in June. Improved macro sentiment supported zinc prices, which closed up 1.21% for the month.

Overall, in the first half of the year (H1), the weak performance of zinc prices was mainly driven by concerns over trade prospects brought about by tariff policies and expectations of a supply-side surplus.

Looking ahead to the second half of the year (H2), as July approached, tariff uncertainties resurfaced. Trump announced that he would impose tariffs on countries that had previously been exempt from tariffs starting August 1. Market expectations for interest rate cuts weakened. Meanwhile, the Sixth Meeting of the Central Financial and Economic Affairs Commission was held, emphasizing "regulating enterprises' low-price and disorderly competition in accordance with laws and regulations, and promoting the orderly exit of backward production capacity." Market sentiment improved somewhat. On the ore side, despite disruptions at Kipushi in Q2, the annual zinc production guidance remained unchanged at 180,000-240,000 mt in metal content. The Huoshaoyun mine continued to ramp up production, bringing a significant increase in domestic zinc ore output. Additionally, June marked the tail end of production resumptions at domestic zinc ore mines. Considering the seasonal pattern of domestic zinc ore operations, production at these resumed mines continued to recover in Q3, while Q4 coincided with the peak maintenance period for domestic zinc ore mines. Coupled with the temporary shutdown of some northern mines at year-end, it is expected that domestic zinc ore production will increase first and then decrease in H2, possibly reaching its annual peak in July/August. The domestic zinc ore market supply will remain consistently adequate. Regarding zinc prices, considering the fluctuations in macro sentiment and the uncertainty surrounding the US Fed's interest rate cuts, SMM expects that the center of zinc prices may decline slightly in H2.

(The above information is based on market collection and comprehensive assessment by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.)